It is interesting how herd investing and recency bias works. People often make poor investment decisions because they "Follow the Herd" and do what everyone else is doing and most people think what has recently happened will continue to happen forever.

In the last few years more and more people have been flocking out of stock/equity markets. Often when investors flock out of an investment class it presents the ideal time to start investing in that area, provided the investment class is sustainable.

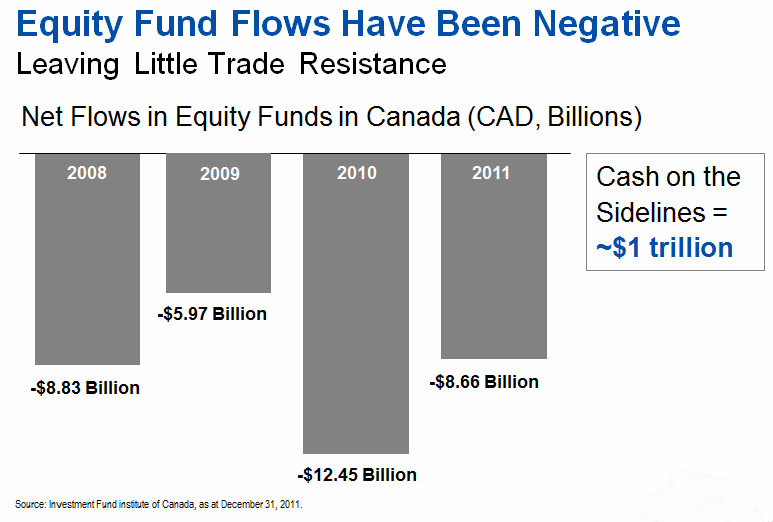

Check out this interesting chart showing the flow of money out of the markets since 2008.

When people leave the markets they settle for more conservative or "Guaranteed" investments like Money Market Funds, GIC's or Government Bonds. The issue at hand is that these investments don't provide enough return to even keep pace with inflation. In a retirees case, this income is often not enough to keep pace with their lifestyle.

BUT...most people keep on investing in this way because they think that "The markets are too scary and they never make any money".

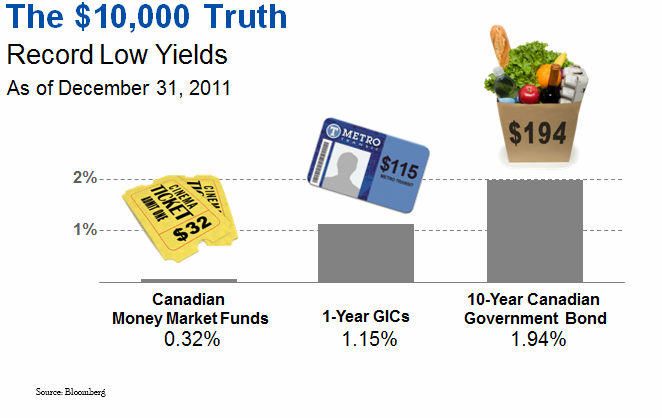

So what do people get in return for being apprehensive? They get paid record low incomes on their investments.

Lets look at some real life examples of what the income from these investments will provide you.

Please note we have not included tax in the following examples:

In this case, an investor who puts forth $10,000 of their capital will earn enough money on his/her investment to purchase;

1) $32 trip to the movies.

2) $115 one month metro pass.

3) $194 enough to buy a few weeks groceries.

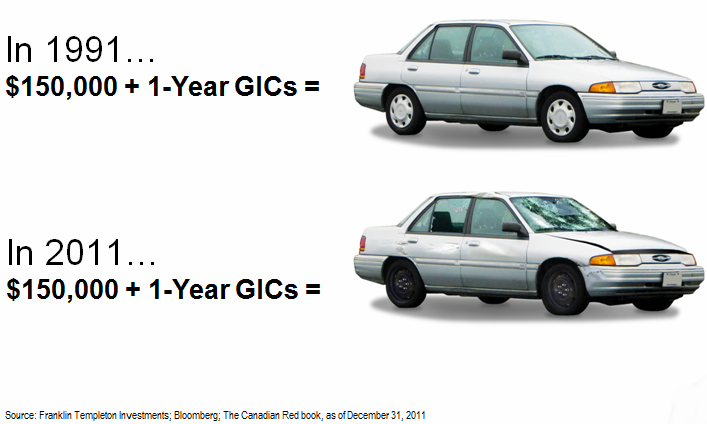

I personally like this example more!! Interest rates/Income providing rates havent always been at all time lows. This example shows us that;

- $150,000 invested in a 1yr GIC in 1991 would provide enough return to buy a 1991 Ford Escort.

- $150,000 invested in a 1yr GIC in 2011 would provide enough return to buy a used 1991 Ford Escort.

A simple solution

Use Liability based investing. Invest your money depending on how you will need your capital.

- If we know we need money soon (1-3 yrs), we invest in short term liquid securities.

- If we need money in a few years (3- 8yrs) we invest in investments that will offer a higher rate of return over this period of time.

- If we have money that we won't need to see for 8 years+ then we can invest in longer term securities and not have to worry about what happens in the markets.

This solution basically places your investments in different baskets based on future liabilities. This approach allows you to shift your focus on how you think about investing in markets and taking risk with your money. Rather then putting all your money in something that will return very little because you are concerned about markets you can allocate your money to different investments based on when you will need the to use the money.

---

When dealing in financial matters, you are urged to consult an advisor for legal, tax or investment advice. Every effort has been made to present information in a clear, exacting manner. However neither the publisher nor the authors can be held responsible for any losses incurred due to the actions of any individual as the result of this post or any errors or omissions contained herein.

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here