1) Money needs a name: Money is fluid and always moving, that’s why we call it “currency.” If you don’t put a name to it or label what it is meant to be used for, it will find somewhere to go. We need to remember this and set up automatic plans to take care of the Nnumber One person (you). This has been preached over and over … and it is true: Pay yourself first.

If you have money sitting in your chequing account, you will spend it, and if you keep your savings account in the same bank you may also easily access it. We recommend setting up a savings account elsewhere that puts an obstacle in between you and your money.

If you save money on for instance a utility bill , it feels good like getting a raise at work. But after a month or so, you don’t realize the difference. You need to redirect that money somewhere right away, perhaps to your savings account.

2) Insurance is simply buying money at a discount: You may not really need life insurance today, but one day you might. And at that time, you may not be able to get it. I have seen more people getting declined than approved for life insurance last year.

At the end of the day, life insurance is money — money that will pay out more than what youpaid for it. If later you don’t want the policy, have someone else pay

the premiums for you, and they get the benefit. Think about what it costs to insure your car, then think about what it would cost to insure your ability to earn or replace your income.

All life insurance is, is guaranteed tax- free money at a discount (see the example at the end of this post).

The same applies to Critical Illness or Disability Insurance.

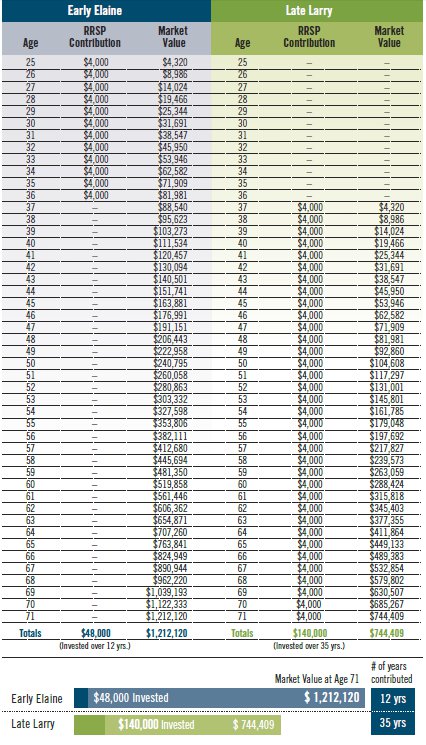

3) Time has the biggest impact on your investment portfolio: If we look at what impact 10 years of time earning a return makes, there is an exponential increase in the value of that portfolio. In the formula for calculating the future value of an investment, themost important factor is time. People often spend too much time trying to figure out how or where to invest, or they keep putting off the decision. The best thing to do is to just make a decision and start investing.

Use a monthly contribution and live and learn, you can always make changes later. Saving $200 a month for 25 years at 7% will give you roughly $157,500.

(See the Late Larry and Early Elaine example at the bottom of this post.)

4) Debt needs a strategy: Don’t get stressed out and let debts run your life. Have a real strategy for getting rid of debt. Review the strategy once a month and adjust it accordingly. You don’t need to think of it every day, but you do need to have a strategy , review it and stick to it.

Here are some examples of strategies for getting rid of debt:

Dave Ramsey's Debt Snowball

Debt Snowball Calculator

7 Debt Reduction Strategies by Zilchworks.com

5) Your behaviour: Like many things in our life, our emotions cause us to make many of our decisions. Unfortunately, when we are anxious and stressed, we make our worst decisions. If we don’t take hold and think logically about our finances, we make stupid decisions. If you don’t know what to do, get help from a professional; but most of all, be aware of what your feelings and try not to make big decisions quickly. Think rationally.

Appendix

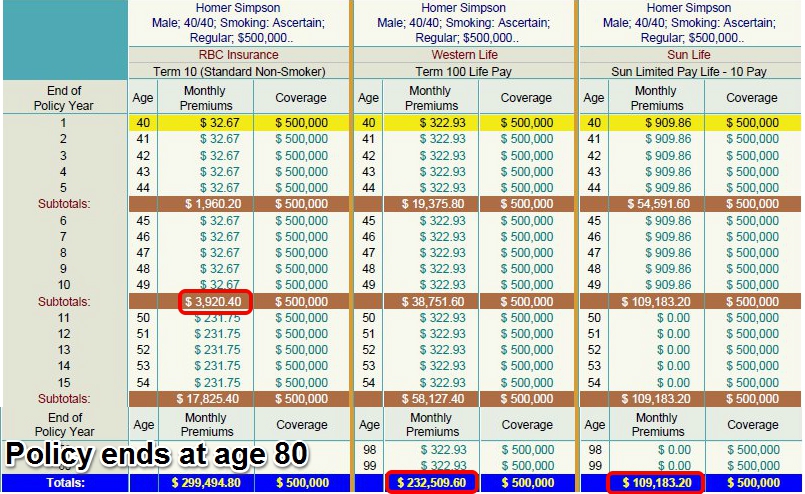

Life Insurance is money at a discount. Below is an example of a 40year old male non-smoker in of regular health looking for $500,000 of life insurance. The Chart shows a Term-10 on the left, followed by a Term-100 and a 10-Pay insurance policy. It has been adjusted to show the first 20 years of the policy and the last two years of the policy. In the Term-100 and 10-Pay examples, we see that if Homer Simpson lived until the ripe age of 100, he would still pay have paid significantly less than the $500,000 benefit. In the early years of the Term-10, Homer pays a huge discount for his money. Don't forget also that this benefit is after tax.

Late Larry Early Elaine

This example assumes an 8% annual rate of return.

---

Infinite Financial is an independently owned and operated Financial Services company in Barrie, Ontario. We specialize in Life Insurance, Retirement Planning and Estate Planning.

Our Certified Financial Planners represent the major Banks, Investment, and Life Insurance companies in Canada. We pride ourselves in offering advice independent of any particular Life Insurance, Bank or Investment firm and based strictly on client’s needs.

Contact us today or stop by our office in Barrie to say Hello!

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here