The pure purpose of Estate Planning is to make an efficient transfer of wealth. Efficiency of Estate Planning is measured in two parts:1) Tax: It is important to plan your estate in a way that will transfer wealth in a tax-efficient manner—set...

Ask an advisor:

One of our advisors will reply as soon as possible. We treat you like family and we don't spam family.

How to Save the Family Cottage

We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talk...

How Mutual Fund Fee's Work

Mutual Funds have become a real point of contention in the media in the last few years. I recently watched a “CBC Market Place” report where a woman went to several financial institutions and asked “how do the fees with mutual funds work?”.

I was both shocked and amazed with how difficult this question was for these professionals to answer, and since then I’ve noticed from reading several articles and blog posts that these professionals and this client was not alone. To see the video - Click Here

So I would like to clear the fog and put it all out there.

First thing that is very important to understand is that Mutual Fund Fees are directly related to how investment advisors, and investment managers get paid. “How we get paid/Our business model” is really a conversation that needs to be had early in your financial advisor relationship. This should be done in your first meeting and be re-iterated in your letter of engagement.

It is also important to understand that depending on the structure of the financial advisors business model, there is a few different ways that you can be charged.

I will do my best to explain the most common ways mutual funds are set up. If you would like clarification, please don’t hesitate to ask.

Other versions – To keep things simple…I am going to share a few core examples. There are other structures out there that are derivatives of my examples that benefit different situations like non-registered money, and used often with higher value account sizes. To see a great further explanation on the variety of these structures- Click Here

There are two types of fees that can be associated with mutual funds – Sales Fees and Management Fees.

Let’s use a very simple example. You have decided that you want to invest your $100,000 in XYZ Equity Fund. Next step is to decide how this account will be managed based on the model of the advisor.

Mutual Fund Sales Fees

Now that we have decided on what you want to invest your $100,000 in, we now need to decide how to structure sales fees. Sales fees are directly related to how the advisor will get paid up front on the transaction.

Option 1 –Back End Load/ Deferred Sales Charge and Low Load (DSC, LL)

In the back end load structure, the fund company will pay the commission dollars to the advisor. The client will then have to pay a fee if they sell and withdraw your money from that fund company within a certain period of time. This varies from company to company, but let me give an example.

Back End Load – Sales Fee Schedule

Year’s | Sales Fee |

1 | 6% |

2 | 5.5% |

3 | 5% |

4 | 4.5% |

5 | 4% |

6 | 3% |

Thereafter | Nil |

So again…You have invested your $100,000 in XYZ Equity Fund, and if you decide to sell and pull your money out of the fund company you will have to pay a sales charge. If you removed your funds in year 5 for example the fee would be $4,000 (4% of $100,000). You can switch funds within the family without incurring fees. This means you could switch from XYZ Equity fund to XYZ Dividend Fund with no fee.

The rational for this fee is because when a purchase is made using the Back End Load structure the Fund Company pays a commission to the Investment Dealer of usually 5%. So the fund company says..

“We paid these people a commission for your business…If you decide to leave within a period of time, we want that commission back”

There is also something called ‘Low Load” which is the same concept but with a shorter time frame, and less fees. Here is an example of a Low Load Structure;

Years | Sales Fee |

First 18 months | 3% |

Between 19 and 36 months | 2% |

Thereafter | Nil |

Low Load works the same way…The Fund Company pays the investment dealer a commission typically of 3% and if the client sells, they want to recoup that commission.

Option 2 – Front End Load (FEL)

Now you can also set up a Front End Load fee. In a front end load the advisor charges the client directly the commission up front typically anywhere from 0% - 5%. If you choose this method, the amount you deposit will be reduced by the fee amount.

For Example: If I charge a 3% FEL fee and you invest your $100,000 in XYZ Equity fund – You would only actually end up investing $97,000 (3% of $100,000).

In this structure there is no other fee if you sell and remove your money from the fund company. You paid the commission directly to the investment advisor, so the fund company will not need to recoup the commission.

Now…Not to add a level of confusion here…But there is one more component that works in the clients best interest if they have chosen the Back End or Low Load structure. Every year you are able to “Free Up 10%” of your fund units and move them to the Front End Load structure, thus eliminating any sales fees on those units.

Using our above example…After year 1 – You could take $10,000 out of back end load and hold the same investment in the front end load version. In year two you could move another 10%.

Mutual Fund Management Fees (MER)

Mutual Fund Management Fees are used to compensate the Fund Company, The Fund Manager, and the Investment Advisor on an ongoing basis for managing, and servicing your account/s.

Whether a client uses front end or back end structure there is typically a service fee or “trailer fee” paid to the advisor. The commission to the advisor is less for Back End Load then Front End Load and ranges from 0% - 1% paid to the dealer depending on the type of investment, Fund Company, etc.

Some of the services that are included in the MER’s range from company to company but in general are the following;

Mutual Fund Company Costs

- Administration Costs

- Trading Expenses

- Portfolio Manager compensation

- Reporting

- Etc.

Advisor Services

- Investment Advice

- Investment Due Diligence

- Tax Planning

- Financial Planning

- Estate Planning

- Retirement Planning

- Portfolio Management

- Economic Research

- Etc.

How MERs are calculated

The MER is calculated daily based on the value of your account.

The formula is - (Account Balance) x (MER) / 365 days

For example - $100,000 x 2%/365 = $5.48

Hypothetically if your manager generated the same return daily as your daily MER at the end of the year your MER cost for the year would be $2000.

This calculation is made daily. If your account drops in value – the fund company and investment advisors pay is dropped and conversely if your account goes up in value the commission increases.

When you look up a mutual fund most of the time performance numbers are posted after fees. So if you see that the mutual fund had an annual return of 8% and an MER of 2% - That means the annual return was 10% (-) 2% MER = 8% net return to the investor.

The MER does allow your fund manager and investment advisor to have a vested interest in the value of your account vs. just charging a flat fee for managing an account. The reason being, if your investment account drops by 50% than the compensation to the professionals also drops 50%.

There is a great calculator on Canada’s Investor Education Website “GetSmarterAboutMoney.ca” that allows you to choose a fund and see the impact. To see the calculator - Click Here

Performance Fees

Certain fund companies (typically Hedge Fund companies) will also charge what’s called a Performance Fee.

This performance fee is intended to further align the interests of the manager with the investor and allow a higher compensation for higher returns. The way a performance fee typically works is the following;

You pay a flat MER and the manager will charge a percentage of outperformance based on a certain benchmark. There is several different formulas for doing this but allow me to share a common example.

2 and 20 – One of the traditional formulas was to charge a flat 2% fee and then 20% of the outperformance of the index.

So let’s say the fund invested in US and Canadian Equities the benchmark might be a 50/50 mix of the S&P 500 and the TSX.

If the fund returned 15% and the blended index returned 10% - The fund companies MER would increase based on the additional 5% of return the company returned over 10%. In other words…they would charge your account a 20% fee on the additional 5% return.

There has been a lot of flak about mutual funds over the years and I can totally understand. A huge issue in this day and age is financial literacy, and quite frankly I don’t believe many investors are being educated about how these things work.

Mutual Funds are not for everybody, and further to that there is somewhere in the neighbourhood of 10,000 mutual funds in Canada most of which add no value to investors (adding performance or reducing risk). It is important to decide what makes the most sense for you, and determine if your Financial Planner/Financial Advisor is getting paid in a way that you feel comfortable with. If their compensation is all derived from mutual fund commissions, it is important that they are providing enough value to your relationship to justify the cost to you.

Again, in this post I have tried my best to keep things clean and simple. There are other derivatives of fund fees and compensation out there. Hopefully your advisor will discuss these different structures with you, especially when it is relevant and in your best interest to utilize. For more information visit this link - Click Here

---

Infinite Financial is an independently owned and operated Financial Services company in Barrie, Ontario. We specialize in Life Insurance, Retirement Planning and Estate Planning.

Our Certified Financial Planners represent the major Banks, Investment, and Life Insurance companies in Canada. We pride ourselves in offering advice independent of any particular Life Insurance, Bank or Investment firm and based strictly on client’s needs.

Contact us today or stop by our office in Barrie to say Hello!

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here

Dont Forget These Two Simple Steps When Estate Planning

The pure purpose of Estate Planning is to make an efficient transfer of wealth. Efficiency of Estate Planning is measured in two parts:1) Tax: It is important to plan your estate in a way that will transfer wealth in a tax-efficient manner—set...

How to Save the Family Cottage

We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talk...

Investment and Market Commentary

The amount of information available in the financial services world is outstanding and overwhelming. It can be frusterating as there are so many contrarian views, and articles written by non-professional writers.

We have comprised some of our more favourite articles and commentary.

Dundee Corporation 2012 Annual Report - The founder of Dundee Ned Goodman is a vetran of the financial business having started Dundee and all the other business that has spurred off of this experience. He has been in the business almost 50 years, and has a very rational and logical way of looking at things. His previous annual reports are also great reads.

The Psychology of Risk: The Behavioral Finance Perspective - How come investors never seem to be able to earn the returns that markets return? Do investments lose money or is it investors that lose money? This is an excerpt from a textbook and is written very factually. Understanding your investor behaviour, and why you feel the way you do about your investments is probobly one of the most important parts of being an investor. Like so many things in life...Step 1 is awareness.

Kyle Bass - Hayman Capital Newsletter - Kyle Bass is one of the worlds most highly respected hedge fund managers. He is known for making bold calls that are unlike the concensus, for example calling the US housing and financial collapse in 2008. He produces several pieces of literature every year. His pieces are very direct and factual, and great for the investor looking for "real" perspective.

Bill Gross, Pimco - Bill Gross is founder and co-chief investment officer of PIMCO one of the largest bond management firms in the world overseeing $1.9 trillion of securities. He brings over four decades of investment experience. He offers monthly market commentary.

- Wounded Heart - June 2013

- The Tipping Point - July 2013

- Bond Wars - August 2013

- Seventh Inning Stretch - September 2013

- Survival of the Fittest - October 2013

The Canso Investment Px - Canso Invetsment Counsel Ltd. provides portfolio management services to private and institutional investors. The portfolio managers and analysts at Canso are very experienced in banking and credit analysis. Before they decide on the upside for a stock, income trust, bond or any other type of security, they examine the downside. Liquidity, financial leverage, bank credit and operating efficiency are all examined with an emphasis on the risk of default. This determines the risk of an investment and how much portfolio capital to risk investing in it.

---

When dealing in financial matters, you are urged to consult an advisor for legal, tax or investment advice. Every effort has been made to present information in a clear, exacting manner. However neither the publisher nor the authors can be held responsible for any losses incurred due to the actions of any individual as the result of this post or any errors or omissions contained herein.

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here

Dont Forget These Two Simple Steps When Estate Planning

The pure purpose of Estate Planning is to make an efficient transfer of wealth. Efficiency of Estate Planning is measured in two parts:1) Tax: It is important to plan your estate in a way that will transfer wealth in a tax-efficient manner—set...

How to Save the Family Cottage

We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talk...

Newsletter - October 2012

Here is a fall newsletter produced by our team, and investment dealership Banwell Financial Inc.

“Quietly, ever so quietly corporate earnings in America are going to an all-time high.”

Fred Sturm, Chief Global Investment Strategist Mackenzie Investments 08/12

“If the economy is in recession, or about to enter a recession, it’s certainly not being reflected in any downturn in factory activity in America’s manufacturing heartland, which is experiencing a manufacturing renaissance and does not appear to be anywhere close to being about to fall off a recessionary cliff.”

Norm Lamarche, Principal/Co-Founder Front Street Capital 08/12

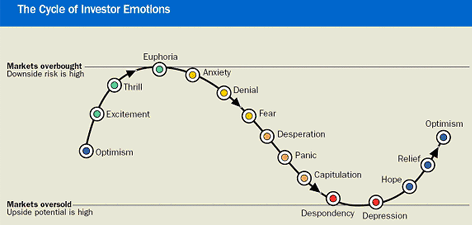

Whether it be the ongoing financial crisis in Europe or the potential economic slowdown of China, we believe, generally speaking, investors over the past year have been focused on the negative headlines taking place.

This negative sentiment is indicated by the US market averages such as the Dow Jones and the S&P 500 not accurately reflecting what is happening to the broad US equity market as indicated by the NYSE advance/decline line reaching a record high level in mid-July. Emotional investing is how most investors end up losing money. See the chart below to find out how investor emotions work through an investment cycle.

We know for certain, markets move in the short term based on emotion, but longer term what will drive prices higher are corporate earnings!

In a de-leveraging slow growth economic environment, we believe our paid to wait strategies of owning yield producing assets (corporate bonds, dividends, infrastructure, and real estate) has worked well and is still an excellent place to be.

This strategy targets a 6-7% net yield to the investor and is not dependent on stock market direction to achieve this target. Although not immune from negative headlines, this strategy has provided near equity-like returns with reasonable stability of capital.

For growth oriented investors with a medium term or longer time horizon, we believe the Universal American Growth portfolio from Mackenzie represents excellent growth potential. Phil Taller lead manager of American Growth (ex-Trimark money manager) you may recall, spoke at our client evening at the Cool Beer Brewery years ago.

“There’s a reason why Google, Amazon and Facebook all come from the US. It comes from a spirit of innovation and growth that has been battered by some tough times, but is still head and shoulders above most countries.”

Phil Taller 06/12

Mackenzie Universal American Growth received the Morningstar Canadian Investment Award for best US Small/Mid Cap Equity Fund in 2009 and 2010.We have an excellent Taller summary in our office from one of his recent road trips into the US, please call or e-mail Jessica for your copy (jsaad@banwellfinancial.com).

High Octane Performance

Norm Lamarche lead manager of the Front Street Growth portfolio, believes there is an industrial revolution occurring in America right now. Lamarche asserts there are many concerns surrounding the US, but believes economists are missing the hugely positive underlying themes taking place.

From one of our previous newsletters, you may recall Front Street is incredibly bullish on the US and believe this is the ‘Mother of All Themes in our Lifetimes’. Front Street are thematic money managers who try to identify themes that drive economic activity.

Front Street Growth has been negative over the past year but on average, post drawdown performance one year after, averages in excess of 60%.

As advisors we are pounding the table on this one as we have confidence in the Front Street track record. The timing not only provides us with a margin of safety, but huge upside potential!!

As of August 31st/2012 Lamarche manages the best performing fund in Canada over ten years. See Norms performance below.

Please call our office if you care to discuss or to request Front Street Commentary. To see a recent interview with Norm Lamarch on BNN click here

On a different note, we welcome client commentary, questions, and/or feedback. We are always available for phone, e-mail or coffee conversations and consider this to be part of our responsibility.

We utilize newsletters as our means to summarize money manager commentaries, filter out unnecessary noise from the media, and attempt to offer timely and objective information.

During uncertain economic periods…threats of war, government deficits, banking crisis, elections, we can’t help but reflect that these issues are not new, but are quite similar to issues that we have confronted in the past. Quite often when the world looks so bleak, subsequent equity performance can be substantial.

We do not take your business casually and truly value the opportunity of serving you.

BEST WISHES FOR A SAFE AND HEALTHY AUTUMN SEASON FROM THE ENTIRE TEAM AT BFI

---

When dealing in financial matters, you are urged to consult an advisor for legal, tax or investment advice. Every effort has been made to present information in a clear, exacting manner. However neither the publisher nor the authors can be held responsible for any losses incurred due to the actions of any individual as the result of this post or any errors or omissions contained herein.

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here

Dont Forget These Two Simple Steps When Estate Planning

The pure purpose of Estate Planning is to make an efficient transfer of wealth. Efficiency of Estate Planning is measured in two parts:1) Tax: It is important to plan your estate in a way that will transfer wealth in a tax-efficient manner—set...

How to Save the Family Cottage

We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talk...

The Three M's of Mutual Funds

Mutual funds get alot of flack, and dont get me wrong they should there is a lot of terrible funds out there...

But dont kid yourself, there is also great money managers out there who can do a far better job than you, me, or most stock brokers out there. (dont believe me, come see me and I will prove it to you)

Which brings me to my Three M's of Mutual Funds, to help you figure out which ones make sense for you...

Manager - This in my opinion is most important. The manager is the captain of the ship, the idea guy/gal, the brains of the operation, the professional and who at the end of the day is managing your money. If you are going to get a specialized surgery, are you going to go online and get the easiest, quickest, cheapest surgeon on the market, or are you going to do your research and get the surgeon who has the best track record of long term performance, consistency, and sticks to what he knows?

Mandate - Mutual Funds have to follow certain protocol to be able to pass regulation. Every fund has a mandate of terms that it needs to follow. Some are very loose (manager can invest in anything but not have more than 10% in any one security). Some are tight (fund cant invest more than 10% in any one sector or outside Canada. I personally usually like the first one, but its important to find what matters most for you.

Motto - What is the overal investment firms values, and motto? Do we agree with it and are they going to stick around and continue to thrive? Every firm has beliefs, it is important that those align with yours, and of course they make sense in todays environment.

For a full blown guide on Mutual Funds click here

---

When dealing in financial matters, you are urged to consult an advisor for legal, tax or investment advice. Every effort has been made to present information in a clear, exacting manner. However neither the publisher nor the authors can be held responsible for any losses incurred due to the actions of any individual as the result of this post or any errors or omissions contained herein.

Infinite Financial places mutual fund transactions through Banwell Financial Inc. and Life Insurance transactions through Bridgeforce. To learn more about these relationships - click here

Dont Forget These Two Simple Steps When Estate Planning

The pure purpose of Estate Planning is to make an efficient transfer of wealth. Efficiency of Estate Planning is measured in two parts:1) Tax: It is important to plan your estate in a way that will transfer wealth in a tax-efficient manner—set...

How to Save the Family Cottage

We have all heard the old saying, “Two things are guaranteed in life: 1. Death 2. Taxes.”We are at an interesting time right now where prices of assets over the last 50+ years have seen a tremendous growth spurt. I always find it interesting talk...